President Trump signed H.R. 748 the “CARES Act” into law on March 27, 2020 that stimulates the economy with a $2.2 trillion government subsidy. Among this, individuals will receive an estimated $560 billion. With the rise in unemployment, and concerns regarding creditor-debtor relationships, COVID-19 and the CARES act will have a dramatic impact on those who will file bankruptcy or who are currently in an active bankruptcy. The CARES act makes several temporary changes to chapter 7 and chapter 13 of the Title 11 Bankruptcy Code.

1. Exclusions of the CARES Act emergency payments from the definition of current monthly income.

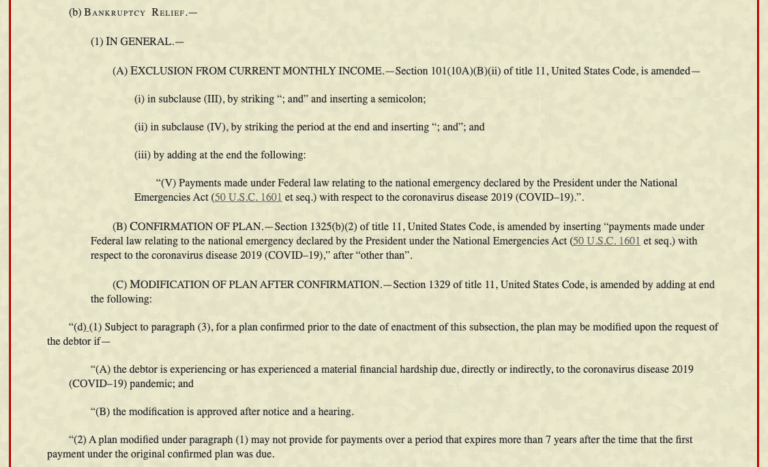

For cases under Chapter 7 and Chapter 13 of the bankruptcy code, the CARES Act expressly modifies in 11 USC §101(10A)(B)(ii) to exclude payments from the CARES Act in the definition of “current monthly income.” This also means that payments from the CARES Act are excluded from the definition of “disposable income” in 11 USC 1325(b)(2) for individuals in active Chapter 13 payment plans. In other words, the CARES Act payments to individuals in open Chapter 13 plans do not need to be paid into their plan.

For individuals filing Chapter 7, the exclusion of the CARES Act emergency payments from the definition of current monthly income means that these payments do not need to be added to the means test calculation in 11 USC 707(b).

2. Modification of Chapter 13 plans and extending plan terms to account for impact of COVID-19

The CARES act modifies 11 USC §1329 to allow a debtor to modify a confirmed plan if “the debtor is experiencing or has experienced a material financial hardship due, directly or indirectly, to the coronavirus disease . . . .” Although it remains untested what a material financial hardship would be, it can be expected to include unemployment, lost hours, and similar foreseeable results from COVID-19.

Modifications under the CARES Act amendments may also extend the life of the plan, though it “may not provide for payments over a period that expires more than 7 years” after the original plan. Presumably, this means that modified plans may allow gaps in payments while the COVID-19 outbreak settles. Although the law has recently been signed by President Trump, there has been little testing about what sort of modification will be permitted by the Courts.

The CARES Act applies to bankruptcy cases filed before during and after its enactment and can have widespread effects on open consumer bankruptcy cases. It remains uncertain how the changes to Title 11 Chapters 7 and 13 will be treated by debtors, creditors, and judges; it remains uncertain how COVID-19 will impact open and to-be filed bankruptcy cases.